Important Accounting Documents You Must Keep in Dubai

Do you know that keeping proper accounting records is essential for your startup’s success and stress-free in Dubai? In fact, it’s a must for staying secure, compliant, and audit-ready. The Federal Tax Authority (FTA) has strict regulations about the audits. If your records are messy or incomplete, you could face penalties, VAT reassessments, or worse, business suspension.

Invy provides a comprehensive bookkeeping checklist for the UAE, ensuring that staying compliant doesn’t have to be complicated. We help you avoid delays and fines and maintain credibility in the best possible way. Contact us today and secure clean paperwork.

In this article, we’ll provide a proper understanding of accounting documents for startups in Dubai to stay one step ahead of your business goals.

Why Recordkeeping in Dubai Really Matters?

In the UAE, maintaining accurate accounting records is a legal requirement. The Federal Tax Authority (FTA) can audit your business at any time. This audit includes checking invoices, contracts, VAT returns, and financial reports to ensure your tax filings are accurate and compliant. The FTA’s enforcement efforts have intensified, making meticulous record-keeping more necessary.

Good bookkeeping is always a strategic advantage for your business. Banks, investors, and potential partners often assess your financials before approving funding. A clean paper trail shows that your business is well-run, financially sound, and trustworthy. Missing records or sloppy organization can damage your credibility. Additionally, maintaining accurate records leads to smoother audits and a stronger foundation for growth.

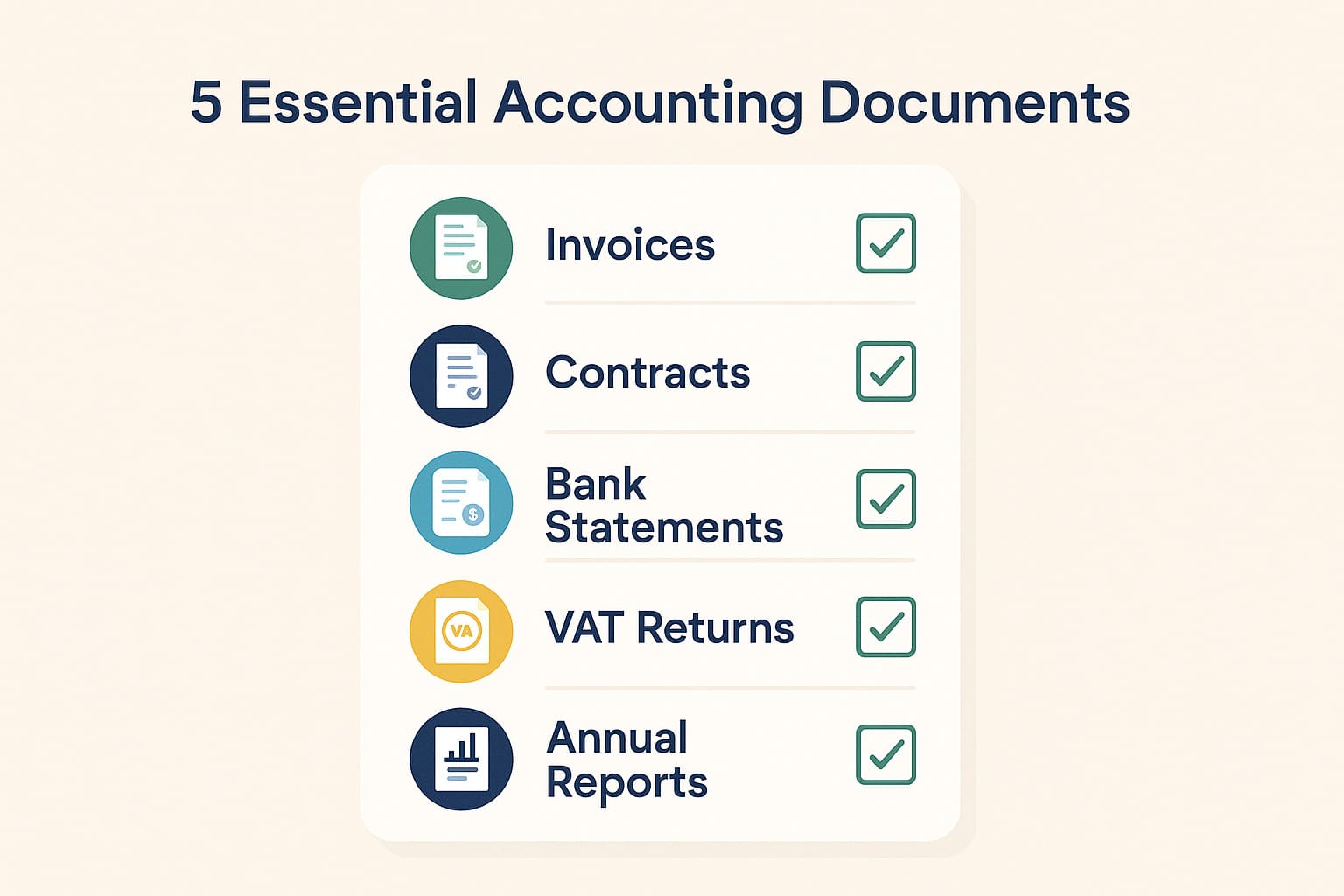

5 Important Accounting Documents in Dubai for Your Business

Smart recordkeeping brings more opportunities for startups. Your bookkeeping checklist UAE helps you build a business that can scale with confidence. Here are

1. Client and Supplier Invoices

Client and supplier invoices provide clear evidence of every transaction. These documents are essential for preparing your VAT returns, reconciling your accounts, or responding to audit inquiries. Also, don’t forget to include credit and debit notes. They adjust invoice amounts and are equally important for tax accuracy.

Consistency matters for issuing digital invoices or using accounting software. You should ensure each invoice includes your TRN, invoice number, date, and VAT breakdown. Missing or incomplete invoices can lead to rejected VAT claims or regulatory scrutiny. Keeping them neatly stored and organized by date or client makes it easier to track payments, manage cash flow, and stay audit-ready.

2. Contracts and Agreements

A signed contract for a service deal, supplier terms, rental lease, or partnership agreement is an essential part of your business. These documents establish the legal foundation for your operations and protect both you and the other party in case of disputes. They also reinforce the legitimacy of the invoices you issue or receive.

The FTA often requests copies of agreements to verify revenue streams, service scopes, or terms related to billing and invoicing. It’s smart to organize your contracts by category and store them with related invoices or payment records. If your business enters into non-disclosure agreements (NDAs), licensing agreements, or distribution contracts, those also count. You can keep both digital and scanned versions, and make sure they’re accessible for at least five years.

3. Bank Statements and Payment Proofs

Bank statements show the actual flow of funds in and out of your account. It must align with your invoices, expenses, and VAT records. FTA auditors often cross-check these statements to ensure reported income and expenses are accurate, especially for high-value transactions.

Therefore, it is advisable to keep proof of payment, such as wire transfer confirmations, online receipts, and cheques. This is especially important when dealing with international vendors or clients. Sometimes, currency conversions or delays can trigger inconsistencies.

To avoid this, you can use consistent naming and filing methods to link payments to specific invoices or contracts. Having a well-documented trail can save you from time-consuming audits or rejected tax claims.

4. VAT Returns and Supporting Documents

Once you're registered, you’re expected to file accurate returns, backed by complete documentation, every quarter. This includes your VAT returns, tax invoices, purchase records, exemption evidence, and credit notes. These files are the core of your tax compliance and must be kept up-to-date and well-organized.

Mistakes or missing documents here can result in significant penalties, delayed refunds, or even suspension. If you’re claiming VAT on inputs, you need receipts that clearly show VAT was charged and paid. Exempt or zero-rated transactions must also be supported with correct evidence. Invy can automate this by storing VAT records, flagging missing items, and preparing you for audits.

5. Annual Financial Reports and Audit Files

Your annual reports can tell the full financial story of your business. These include Profit & Loss statements, balance sheets, trial balances, cash flow statements, and any financial summaries prepared by your accountant or auditor. They give insight into your profitability, risk, and financial health. Data investors, banks, and regulators mostly care about these things.

If your business is audited or applying for funding, these reports will be among the first things requested. They must match your books and reflect your invoices, VAT returns, and bank statements. Having them reviewed by a certified accountant not only boosts accuracy but also reinforces credibility.

How Long Must You Keep Records?

In the UAE, maintaining accurate accounting records is a legal requirement. According to the UAE Tax Procedures Law (Federal Decree-Law No. 7 of 2017) and the VAT Law, businesses are required to retain all relevant financial records for a minimum of five years. This applies to all types of companies, regardless of size or industry. However, if your business is in real estate or deals with capital assets, the retention period increases to 15 years, due to the long-term nature of property and asset transactions.

The documents you need to store include everything from invoices, contracts, ledgers, and expense reports to VAT filings, audit files, and bank statements. These are essential for passing audits, resolving disputes, and filing accurate tax returns. Failure to comply can be costly. The FTA can impose fines starting from AED 10,000 per missing or incomplete record, and these penalties escalate if they affect tax assessments or result in underreporting.

Where to Store Your Records?

In the UAE, digital recordkeeping is encouraged, as long as your documents are secure, readable, and backed up. Many businesses still make the mistake of storing files across email inboxes, desktops, or external drives, which are prone to loss, corruption, or unauthorized access.

While physical copies are legally valid, they come with risks like fire, theft, water damage, or simply getting misplaced, especially as your business grows and the paperwork stacks up. You can also switch to a cloud-based storage solution that centralizes all your files in one place. This makes it easier to organize, search, retrieve, and protect your financial records.

With platforms like Invy, you get bank-level security, automatic backups, and compliance-ready access, ensuring your records are safe and ready for audits at any time. In today’s digital world, going paperless is a secure and efficient strategy.

How Invy Makes Recordkeeping Effortless and Audit-Ready

Designed specifically for UAE businesses, Invy takes the guesswork out of document management and turns chaos into clarity. Here's how:

All-in-One Cloud Storage: Upload and organize invoices, contracts, VAT returns, and more in one secure dashboard, eliminating the need to dig through emails or folders.

FTA-Compliant File Formatting: All documents are saved in a format that meets UAE legal and audit standards. This way, you're always prepared for inspections.

Automated Alerts and Reminders: Get real-time notifications for upcoming VAT deadlines, document expirations, or missing files. You can stay ahead without stress.

On-Demand Expert Review: Connect with qualified accountants who review and validate your records to ensure full compliance and audit readiness.

Secure, Accessible, and Searchable: Access your records from anywhere, anytime—with bank-level encryption and smart search features.

No Guesswork, No Penalties: Invy handles the fine print so you can focus on scaling your business, not chasing paperwork.

Built for UAE Businesses: Designed specifically to align with local tax laws, licensing authorities, and business practices in Dubai and beyond.

Make Recordkeeping Your Business Strength Now!

In the UAE’s fast-paced and compliance-driven environment, maintaining a flawless record-keeping system is a competitive edge. Well-organized accounting documents protect you from penalties, boost your financial credibility, and set the stage for sustainable growth. Your numbers need to be airtight and ready to show when navigating tax season or preparing for expansion.

Invy is your all-in-one platform that takes the stress out of compliance by automatically storing, organizing, and monitoring every critical document. No more missed deadlines, manual tracking, or scattered spreadsheets. Just smooth, secure, audit-ready bookkeeping that works behind the scenes while you focus on building your business. Contact us today to stay one step ahead and handle your recordkeeping with confidence.

FAQs

1. What accounting documents are legally required in the United Arab Emirates?

You must keep invoices, contracts, bank statements, VAT returns, financial reports, and audit files. These are essential for tax filings, audits, and legal compliance with FTA regulations.

2. How long should I store my accounting records in Dubai?

Most businesses are required to retain records for at least five years. For sectors such as real estate or capital assets, the period extends to 15 years.

3. Are digital copies of accounting documents acceptable in the UAE?

Yes, digital records are fully acceptable if they are secure, accessible, and tamper-proof. Cloud storage platforms like Invy meet these legal standards.

4. What happens if I lose or fail to present accounting documents during an audit?

Failure to produce required documents can result in fines starting from AED 10,000 per missing file, and penalties increase if it affects your tax accuracy.

5. How does Invy help with recordkeeping and FTA compliance?

Invy offers secure cloud storage, FTA-compliant formatting, automated alerts, and expert file reviews. It makes it easy to stay organized, audit-ready, and compliant with legal requirements.